Low or Incomplete Scope of Loss

Carriers may overlook hidden damage, downplay escalation, or limit scope to control payouts.

→

Services / Insurance Recovery

We help entrepreneurial property owners recover the full value of their loss across complex commercial and mixed-use assets.

Common Insurance Pressure Points

Carriers may overlook hidden damage, downplay escalation, or limit scope to control payouts.

Outdated unit costs, incorrect adjustments, and inappropriate depreciation can reduce the true cost to repair.

Tactics that prolong resolution, shift blame, and create cash-flow pressure for property owners.

Our Approach

We build the case for full recovery through data, documentation, and strategic negotiation, so the owner can focus on the asset and the business.

Why It Matters

Contingency Representation

Burnside Property & Project Claims handles accepted insurance recovery matters on a contingency basis. That means the firm’s fee is tied to recovery. In plain terms, there is no fee unless we recover money for you.

What We Review

Every property, policy, and loss is different. Our review focuses on the documents, costs, coverage, and facts that affect recovery.

We analyze the policy word for word to identify applicable coverage and recovery paths.

We document the full extent of damage and establish cause, timing, and repair connection.

We test pricing, depreciation, escalation, labor, market rates, and cost-estimating assumptions.

We look for required upgrades and compliance costs that may be overlooked or minimized.

We pursue covered categories that affect the owner’s real recovery, including time-sensitive impacts.

We connect estimates, plans, expert reports, communications, and repair sequencing to the claim.

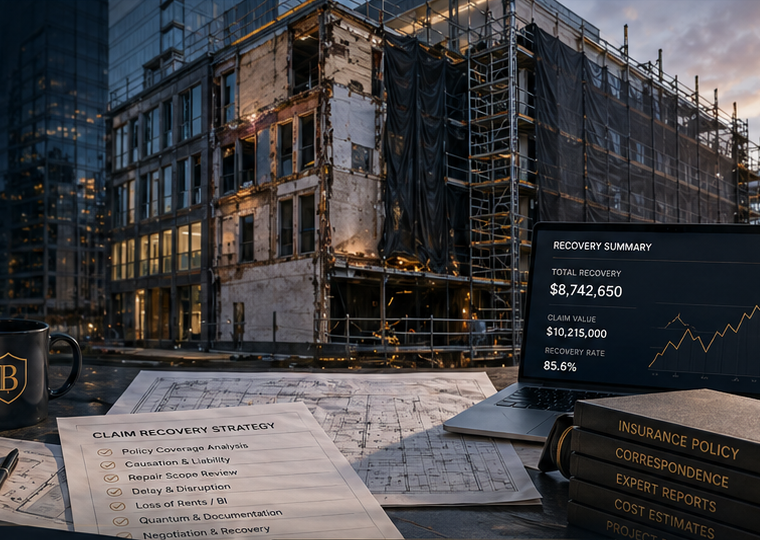

Representative Results

Representative matters only. Every case depends on its own facts, evidence, timing, coverage, contracts, and applicable law. Past results do not guarantee future outcomes.

Unapproved change orders, defective work, delay, and lost rental income were all in play.

Structural instability, foundation reconstruction, stabilization, collateral repairs, and rent loss.

Through trial, arbitration, and settlement in serious owner-side property disputes.

Next Step

Send a short summary before repair decisions, claim positions, or project deadlines narrow your options.

Contingency representation. No fee unless we recover money for you.

Burnside Property & Project Claims is part of Burnside Law Firm. Representative matters are not guarantees. Accepted matters only.